| Want to send this page or a link to a friend? Click on mail at the top of this window. |

More Special Reports |

| Posted September 9, 2009 |

| National |

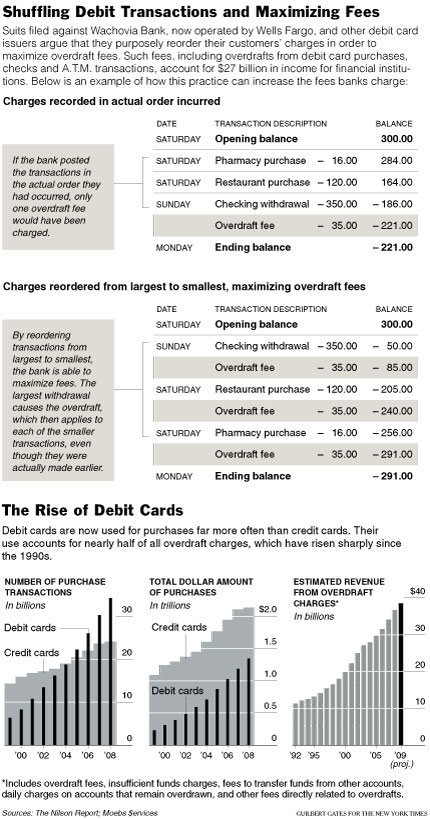

| Overspending on Debit Cards |

|

Is Painful, but Not for Banks |

|

|

LAURA PEDRICK FOR THE NEW YORK TIMES |

| above, has filed a lawsuit against Wachovia Bank. The suit charges that the bank reorders debit card transactions in order to maximize the overdraft fees they can charge. |

|

By RON LIEBER |

|

and ANDREW MARTIN |

|

|

MATTHEW STAVER FOR THE NEW YORK TIMES |

| Peter Means's bank charged him seven $34 fees to cover seven purchases when there was not enough cash in his account, notifying him only afterward. |

|

|

|

|

| A Source of Easy Money |

| 'I Can't Afford That' |

| The Debate in Washington |

| Wehaitians.com, the scholarly journal of democracy and human rights |

| More from wehaitians.com |